Last month we talked about seasonality and how we might need to get past Valentine’s Day to have a good understanding of what was going on in the housing market (February Economic Update). To quickly recap, most markets in the U.S. see a great reduction in inventory going into November and this tends to linger roughly until Valentine’s Day. Then inventory levels tend to tick up going into March Madness and do so in earnest by May/June. Let’s take a peek at the data and examine this more closely.

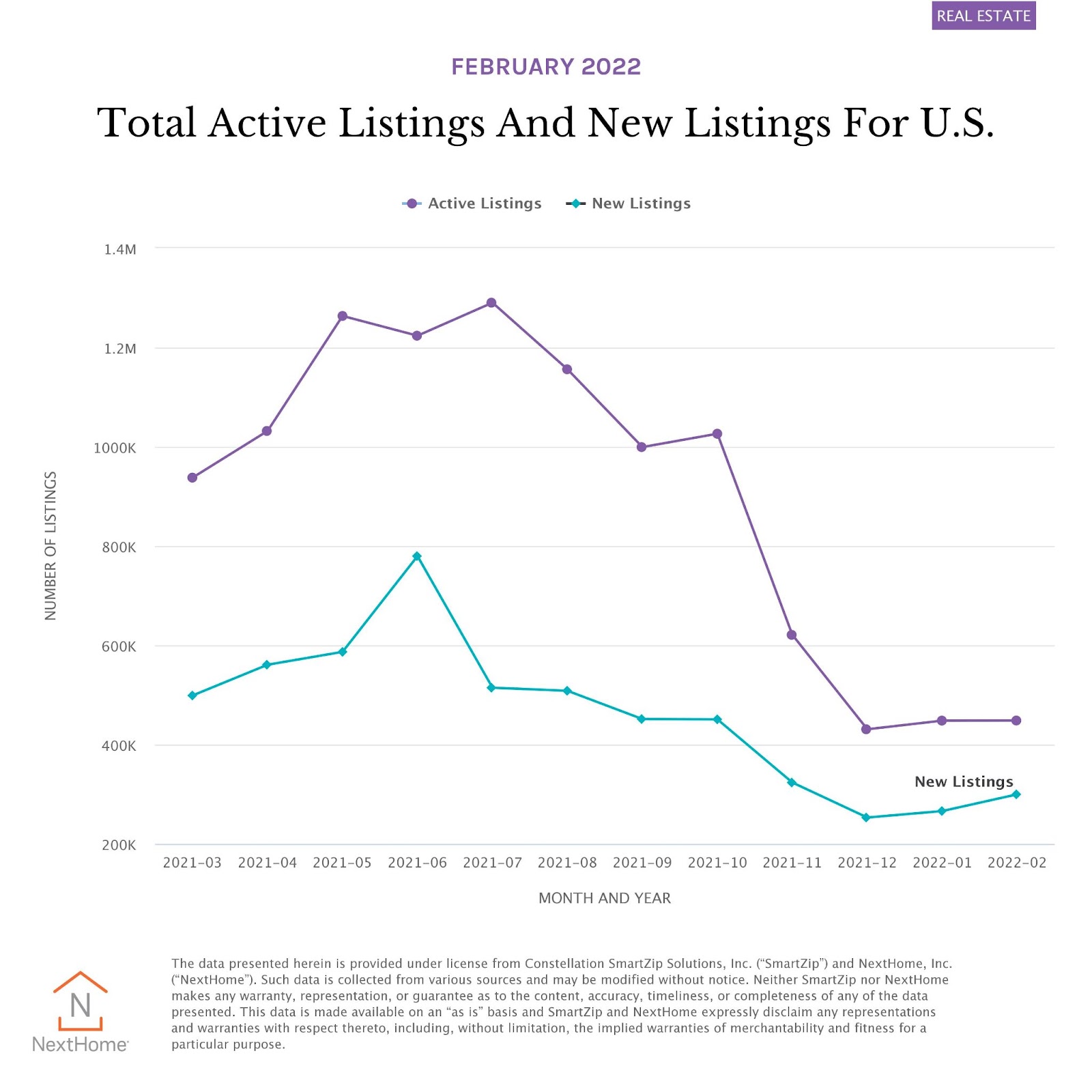

Here we can see the active listings in the U.S. remain flat. It means there are as many homes for sale in February as there were in January. The silver lining here is in the uptick in New Listings. Seeing some upward pressure on that number (11.2%) which could be a leading indicator that we’re starting to see the seasonality taper off and inventory coming onto the market. The reason it stays level for “active listings” is due to buyer demand being extremely high – all that new inventory is being absorbed quickly by buyer demand.

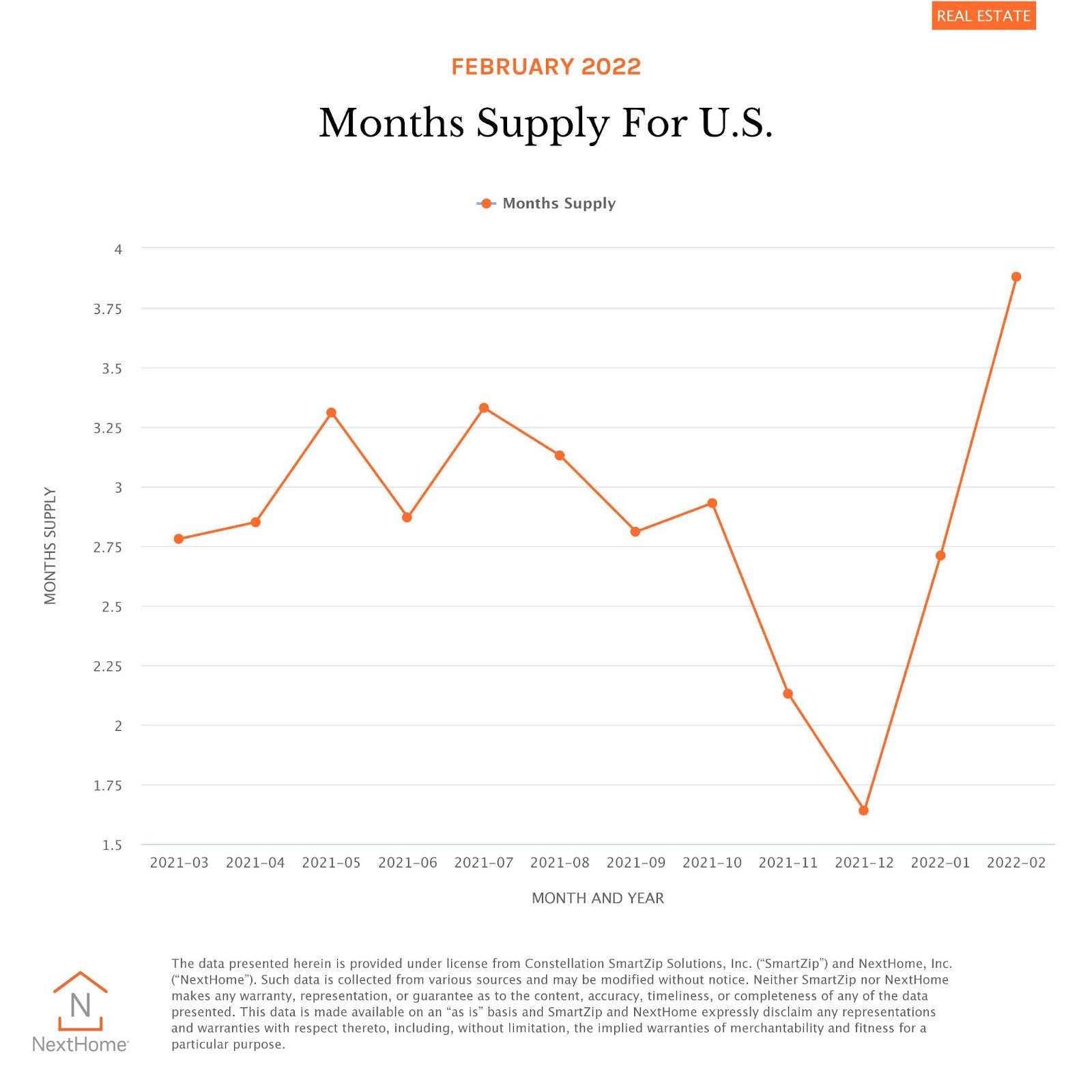

The Months Supply chart really seems to tell the story. You see the dramatic drop in November and December, then the uptick in January, followed by a strong rally in February (a 30% increase in the month). This is a classic seasonality trend line where supply goes from an intensely low level to a somewhat more normalized level. The key to how slow of a slowing market we might experience will be to see what happens next month. We’ll be keeping a close eye on the steepness of this trend line.

To sum up, inventory is on the rise, but it’s not enough to meet buyer demand.

Stay tuned next month when I think we’ll have some real insight into how the rest of 2022 is going to shape up as far as market stats, inventory, demand, interest rates, and other key factors.